Features

Tech Trend Digital Twin Technology in Maritime Operations: Optimising Fleet Performance

In an era where data and digitalisation are reshaping global industries, the maritime sector is undergoing a technological transformation driven by digital twin technology. At its core, a digital twin is a virtual, real-time replica of a physical asset—such as a ship, engine or port infrastructure—powered by continuous data from sensors and advanced analytics. In the maritime context, this technology is rapidly evolving from a futuristic concept into a practical tool that enhances decision-making, efficiency and sustainability across fleet operations, port logistics and vessel maintenance.

What Is a Digital Twin and Why It Matters

A digital twin functions as more than a static model; it is a dynamic system that mirrors the physical counterpart’s condition at all times. It integrates real-world sensor data, navigational logs and performance metrics into a coherent digital platform that updates in real time. This synchronization enables operators and managers to monitor vessel health, simulate “what-if” scenarios and make proactive operational decisions with confidence.

Digital twins differ from traditional models because they are connected to actual assets, and evolve as those assets change, giving stakeholders a continuously accurate and actionable digital mirror. The result is improved visibility and responsiveness across all stages of a vessel’s lifecycle—from design and construction to operation and maintenance.

Enhancing Maintenance and Predictive Analytics

One of the standout capabilities of digital twin technology is predictive maintenance. Instead of relying on fixed service schedules, fleet managers can monitor real-time data from engines, propulsion systems and structural components to identify early signs of wear or impending failure. This allows maintenance teams to act before issues escalate, reducing unplanned downtime and extending the service life of critical equipment.

For instance, continuous real-time monitoring can detect subtle anomalies in engine performance or hull integrity, prompting targeted interventions that minimise disruption and reduce lifecycle costs. By analysing trends and patterns over time, digital twins help shift maritime operations from reactive fixes to proactive care.

Operational Efficiency and Fuel Optimisation

Beyond maintenance, digital twins offer significant benefits in fuel and route optimisation—an essential consideration given volatile fuel prices and tighter environmental regulations. By simulating different routes, weather conditions and engine settings, digital twins can identify the most efficient operating profiles for any voyage. This not only lowers fuel consumption but also contributes to reduced emissions, aligning with broader sustainability goals in shipping.

Port operations also benefit from digital twin technology. Virtual models of port infrastructure, including cranes, berths and storage areas, allow operators to experiment with logistics strategies in a risk-free digital environment. This can streamline processes such as berthing sequences, cargo handling and turnaround planning, ultimately reducing congestion and enhancing throughput.

Safety, Simulation and Strategic Decision-Making

Digital twins also elevate safety and risk management. By simulating emergency scenarios, such as equipment failures or extreme weather events, operators can test responses and build robust contingency plans without real-world risk. This proactive approach improves crew preparedness and enhances compliance with global safety standards.

Moreover, advanced digital twin models can integrate artificial intelligence and machine learning to predict future scenarios and recommend optimal actions, further strengthening strategic decision-making across fleets and ports.

The Road Ahead

The adoption of digital twin technology in maritime operations is still evolving, but its impact is clear: better maintenance regimes, heightened operational efficiency, reduced emissions and stronger safety protocols. As sensors and analytics become more sophisticated, the digital twin will continue to unlock new levels of performance and resilience for fleets and ports alike.

In a world where maritime competitiveness increasingly depends on smart, data-driven solutions, digital twins are poised to become a cornerstone of modern fleet management and maritime innovation.

Asia’s Container Port Dominance: Navigating Congestion, Tech, and Geopolitical Tensions

In the heart of global trade, Asia’s container ports stand as colossal gateways, handling over 60% of the world’s container throughput and fueling the engines of international commerce. From the bustling docks of Shanghai to the strategic hub of Singapore, these ports are not just logistical lifelines but battlegrounds for efficiency, innovation, and power plays. As Bangladesh’s Chittagong Port climbs the ranks amid regional growth, the sector grapples with chronic congestion, rapid technological adoption, and escalating geopolitical risks. This feature unpacks how Asia maintains its iron grip on container dominance while steering through turbulent waters, drawing on recent data and scholarly insights to reveal the high-stakes navigation ahead.

The Powerhouses: Asia’s Top Ports and Their Meteoric Throughput

Asia’s ports have shattered records in 2025, with combined throughput surging amid post-pandemic recovery and e-commerce booms. Shanghai, the undisputed king, crossed the 50 million TEU mark by November, ending the year at an estimated 55.06 million TEUs—a 6.9% year-on-year leap. Singapore follows closely with 41.1 million TEUs, leveraging its transshipment prowess to connect East Asia with global routes. Ningbo-Zhoushan and Shenzhen round out the top tier, benefiting from China’s export surge despite U.S. tariffs. In Southeast Asia, ports like Port Klang in Malaysia and Vietnam’s Cai Mep-Thi Vai are rising stars, driven by nearshoring trends.

Bangladesh’s Chittagong Port, handling around 3.5 million TEUs in 2025, plays a pivotal role in South Asia, serving as a key node for garment exports and imports. However, it’s overshadowed by giants, with throughput growth hampered by infrastructure limits. Globally, Lloyd’s List reports the top 100 ports moved 743.6 million TEUs in 2025, an 8.1% increase, with Asia claiming nine of the top 10 spots.

To illustrate the hierarchy, here’s a table of the top 10 Asian container ports by 2025 throughput:(Data compiled from Lloyd’s List, UNCTAD, and port authorities; estimates for full-year 2025.)

This dominance stems from massive investments: China’s ports alone handled record volumes despite external pressures, underscoring Asia’s resilience.

The Congestion Crunch: Bottlenecks in the Supply Chain

Congestion remains a thorn in Asia’s side, exacerbated by feeder capacity shortages and yard overflows. In Southeast Asia, tight feeder networks have caused transshipment delays and rolled cargo, spiking yard density. Scholarly studies highlight how port congestion inflates containership freight rates, with Asia’s hubs most affected—a 1% congestion rise can hike rates significantly. For instance, a 2025 analysis models congestion’s impact on networks, noting Southeast Asian ports’ vulnerability due to rapid expansion and environmental pressures.

Technology offers relief: Automation at Singapore’s Tuas Port and AI-driven scheduling in Shanghai reduce dwell times by up to 30%. Yet, as a Cardiff University thesis on global congestion notes, Asian ports (38% of studied cases) face unique challenges from typhoons and labor shortages. Bangladesh’s Chittagong, plagued by berthing delays, could learn from these, with proposals for digital twins to optimize flows.

A table of congestion impacts in key Asian ports (2025 estimates):

(Based on JOC and scholarly models; higher index indicates worse congestion.)

Geopolitical Storm Clouds: Tensions Reshaping Trade Routes

Geopolitical frictions are redrawing Asia’s maritime map. The Red Sea crisis has disrupted container calls, forcing reroutes around Africa and inflating costs by 20-30%. In the South China Sea, tensions between major powers threaten key chokepoints, potentially collapsing supply chains. Scholarly work simulates waterway closures in Southeast Asia, estimating trade losses up to 10% for affected nations. Geopolitical risks also spill into volatility for shipping and oil markets.

For Bangladesh, Bay of Bengal dynamics—tied to India’s Belt and Road counter-initiatives—amplify vulnerabilities, with 90% of trade seaborne. A study on Indo-Pacific strategies warns of fragmented ASEAN unity and non-traditional threats like cyber attacks on ports. Mitigation lies in diversified routes and tech resilience, as ports become “key agents or sitting ducks” in tense environments.

As Asia’s ports evolve, balancing dominance with sustainability will define the next decade. For Bangladesh, integrating into this network via upgrades could unlock billions in trade.

1. Lloyd’s List One Hundred Ports 2025 – https://www.lloydslist.com/one-hundred-container-ports-2025

2. UNCTAD Container Port Throughput – https:// unctadstat.unctad.org/datacentre/dataviewer/US.ContPortThroughput

3. Measuring the impact of port congestion on containership freight rates – https:// www.sciencedirect.com/science/article/pii/ S2666822X25000024

4. Geopolitical tension and shipping network disruption: Analysis of the Red Sea crisis – https:// www.sciencedirect.com/science/article/abs/pii/ S0966692324002138

5. The Geopolitics of International Trade in Southeast Asia – https://keremcosar.uvacreate.virginia.edu/ publications/Cosar_Thomas_Geopolitics_SEAsia.pdf

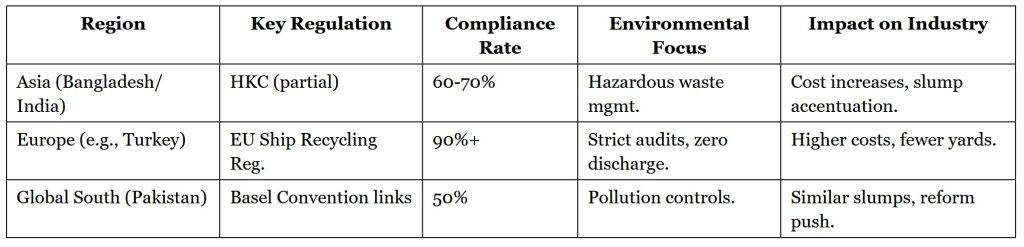

The Ship Recycling Slump: Reviving Bangladesh’s Industry in a Regulated Global Era

Bangladesh’s shipbreaking yards in Chittagong once buzzed with activity, dismantling hulking vessels and supplying steel to a booming economy. But a confluence of global disruptions, stricter regulations, and environmental scrutiny has triggered a slump, with imports dropping sharply. As the Hong Kong Convention reshapes the industry, this feature explores the decline, its impacts, and pathways to a greener revival—spotlighting scholarly evidence on pollution’s toll and strategies for sustainable reform.

The Decline: From Boom to Bust in Ship Recycling Volumes

Bangladesh has long dominated ship recycling, accounting for up to 40% of global volumes by gross tonnage. In 2025, it recycled 2.74 million gross tonnes, retaining its top spot for the seventh year. Yet, the slump is evident: Ship imports fell to 130 in 2024, a 23.5% drop from 170 in 2023, driven by high scrap prices, supply chain issues, and regulatory pressures. Annually, 250-270 ships generate USD 75 million in duties, but volumes have dipped amid COVID aftermath and geopolitical shipping reroutes.

Scholarly reviews trace this to overcapacity and global shifts, with Bangladesh’s yards facing competition from India and Pakistan. The industry supplies 60% of local steel raw materials, supporting 200,000 jobs, but the downturn threatens livelihoods.

A table of Bangladesh’s ship recycling volumes (2020-2025):

(Data from UNCTAD, NGO Shipbreaking Platform, and local reports.)

Environmental Toll: Pollution and Ecosystem Damage

The slump masks deeper issues: Shipbreaking’s environmental footprint. Yards release toxins like heavy metals, PCBs, and asbestos, contaminating soils, waters, and air in coastal zones. Studies show river discharges near Chittagong exacerbate pollution, harming biodiversity and leading to fish extinctions. A 2025 analysis links activities to “more-than-economic dispossession,” where toxins disrupt local commons and health. Welding and sandblasting generate dust that poses long-term risks, with contamination rates in Sitakunda far exceeding safe levels.

Worker safety is dire: Surveys across 18 yards reveal high accident risks, with mitigation proposals urging better PPE and zoning. Global comparisons highlight Bangladesh’s pre-2015 unregulated era caused extensive ecosystem loss.

The Regulatory Reckoning: Hong Kong Convention’s Ripple Effects

The Hong Kong Convention (HKC), effective June 2025, mandates safe, green recycling—yet Bangladesh missed implementation deadlines, risking yard closures. It aims to curb hazards, but critics argue it falls short, as yards circumvent rules via flags of convenience. Three months in, HKC has improved standards but strained the slump-hit industry with compliance costs. Scholarly evaluations praise its role in elevating Bangladesh’s practices, though full adoption lags.

Revival strategies include green upgrades: KSRM Steel’s model shows eco-friendly dismantling boosts sustainability. SWOT analyses suggest leveraging strengths like low costs while addressing weaknesses in regulation.

A table contrasting regulations:

(From IMO and scholarly sources.)

With targeted reforms, Bangladesh can revive its yards as green leaders, balancing economy and ecology.

Information Sources

- Bangladesh’s Ship Recycling Industry in the Global South –https://www.mdpi.com/2071-1050/17/24/10998

- Ship recycling process in Bangladesh – https://www.sciencedirect.com/science/article/pii/S2405844024153753

- The Impact of the Hong Kong Convention on Ship Recycling – https://www.hklaw.com/en/insights/

publications/2025/09/the-impact-of-the-hong-kong-convention-on-ship-recycling-3-months-in - Evaluation of Environmental Impacts of Ship Recycling In Bangladesh – https://wwwcdn.imo.org/localresources/en/

OurWork/PartnershipsProjects/Documents/Ship%20recycling/WP1b%20Environmental%20Impact%20Study.pdf - UNCTAD Review of Maritime Transport 2025 (via reports on volumes) – Implied from and

Reviving the Oceans: The Rise of the Regenerative Blue Economy

In the vast expanse of our planet’s oceans, a quiet revolution is underway. For decades, we’ve treated the sea as an endless resource—a dumping ground for pollution, a highway for global trade, and a buffet for overfishing. But as coral reefs bleach, fish populations plummet, and coastal communities struggle, a new vision is emerging: the regenerative blue economy. This isn’t just about sustaining what’s left; it’s about actively healing marine ecosystems while fostering equitable growth. Imagine wind farms that double as oyster reefs, women-led cooperatives turning seaweed into livelihoods, and policies that protect small fishers from industrial giants. As we stand on the brink of irreversible tipping points, the regenerative approach offers a blueprint for prosperity that’s as resilient as the tides themselves.

The original push for a “sustainable” blue economy put the ocean on the global map, weaving it into development plans and business strategies. Yet, despite these efforts, degradation persists at alarming rates. Warming waters, plastic pollution, and habitat loss are pushing ecosystems to the edge. But momentum is building. With landmark agreements like the High Seas Treaty entering force in January 2026 and billions pledged at the 2025 UN Ocean Conference, the stage is set for transformation. Drawing from fresh data and on-the-ground stories, this feature dives deep into why regeneration matters—and how it’s already reshaping our relationship with the sea.

The Alarming Pulse of Ocean Health

The ocean covers 71% of Earth, regulates our climate, and supports over 3 billion people for protein and livelihoods. Yet, it’s degrading faster than ever. Overfishing remains a scourge: the latest FAO assessment from 2025 reveals that 35.5% of global fish stocks are overexploited, up slightly from previous years, while 64.5% are fished at sustainable levels—but many teeter on the brink. Coastal habitats, nature’s carbon vaults, are vanishing. Mangroves, which sequester carbon 10 times faster than terrestrial forests, have declined by 3.4% globally from 1996 to 2020, equating to a loss of 5,245 square kilometers. Seagrasses, vital for marine biodiversity and coastal protection, are disappearing at 110 square kilometers per year since 1980, with 29% of known extents already gone.

These losses aren’t abstract—they ripple through economies. Degraded oceans mean fragile supply chains, rising insurance costs from extreme weather, and food insecurity for millions. To visualize the scale, here’s a snapshot of key degradation

metrics:

This table underscores the urgency: without intervention, these trends could erase trillions in economic value and displace

coastal communities.

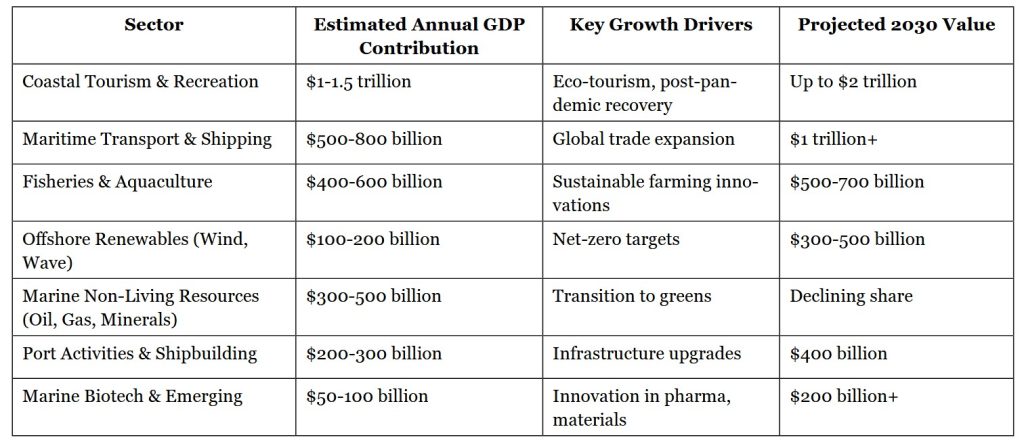

The Economic Engine of the Seas

Amid the challenges, the blue economy hums with potential. Valued at $2.5 to $6 trillion annually—equivalent to the world’s eighth-largest economy—it drives global trade, energy, and tourism. Recent estimates peg it closer to $2.6 trillion, with projections climbing toward $3 trillion by 2030 as sectors like offshore renewables expand. Employment is another bright spot: the ocean economy currently supports over 130 million jobs worldwide, with forecasts predicting growth to 184 million by 2050—a 51 million job increase—if we pivot to sustainability. That’s a 1.5% annual growth rate, outpacing many land-based sectors.

Breaking it down by sector reveals where the value lies. The EU Blue Economy Report for 2025 outlines seven core areas, with coastal tourism and maritime transport leading in GDP contribution. Globally, tourism and recreation alone generate hundreds of billions, while emerging fields like marine biotech and renewables promise exponential growth. Here’s an approximate global breakdown based on recent analyses:

(Data aggregated from OECD, NOAA, and World Bank reports; figures are estimates as global tracking varies.) This table highlights regeneration’s business case: investing in restoration could unlock $10-15 trillion in net benefits by mid-century, creating resilient value chains.

Momentum Builds: From Policy to Practice

The tide turned decisively in 2025. At the UN Ocean Conference in Nice, France, 65 heads of state and 10,000 participants rallied around the Nice Ocean Action Plan—a framework with over 800 commitments and €8.7 billion in pledges for conservation and science.

Record business participation signaled the ocean’s shift to the heart of climate agendas. Complementing this, the Biodiversity Beyond National Jurisdiction (BBNJ) Agreement—aka the High Seas Treaty—entered force in January 2026, governing 60% of the world’s oceans by promoting marine protected areas and equitable benefit-sharing from genetic resources. Meanwhile, the WTO Fisheries Subsidies Agreement, effective September 2025, bans $22 billion in harmful subsidies annually, curbing overfishing and leveling the playing field for small-scale operators.

These policies aren’t just words—they’re catalyzing action. Investor interest spans 70+ ocean innovation categories, from carbon-capturing kelp farms to AI-driven pollution trackers. The World Economic Forum’s Global Future Council on the Regenerative Blue Economy is at the forefront, uniting experts to translate ambition into blueprints. Meeting in Dubai in October 2025, they emphasized cross-sector collaboration, nature-inclusive design, and de-risking investments for local communities.

Stories from the Frontlines: Regeneration in Action

Regeneration isn’t theoretical—it’s happening now. In Chile, Territorial Use Rights for Fisheries (TURFs) empower artisanal fishers to manage coastal zones, leading to rebuilt benthic ecosystems and sustained local economies. After 30 years, studies show higher catch rates in TURFs versus open-access areas, though ongoing monitoring is key to prevent declines.

Across the North Sea, offshore wind farms are morphing into multi-use hubs: RWE’s projects integrate oyster reef restoration and aquaculture, boosting biodiversity while generating clean energy and jobs. A recent feasibility study confirms that just 1% of global wind investments could restore millions of hectares of marine life.

In Zanzibar, Tanzania, women-led seaweed cooperatives like the “Mwani Mamas” are restoring lagoon health while creating income streams. With 88% of seaweed farmers being women, these groups harvest sustainably, produce beauty products, and empower communities amid climate challenges. Ghana’s 2025 Fisheries Act extended the Inshore Exclusive Zone from 6 to 12 nautical miles, shielding small-scale fishers from industrial trawlers and fostering biodiversity recovery.

Beyond these, innovative projects abound: GreenWave’s regenerative ocean farming in the US combines kelp and shellfish to sequester carbon and create jobs. In Europe, EU-funded algae hubs advance sustainable farming, while Mozambique-Tanzania exchanges upskill youth in seaweed cultivation. These examples prove that ecological recovery and prosperity can advance hand-in-hand.

Charting the Future: A Call to Action

As the Global Future Council convenes, the message is clear: regeneration must scale from pilots to norms. By integrating policy, finance, and community co-design, we can build an ocean economy that’s circular, inclusive, and resilient. Governments, businesses, and investors are invited to join— spotlighting initiatives that make regeneration the blue economy’s core principle. The ocean isn’t just a resource; it’s our lifeline. With bold action, we can ensure it thrives for generations, turning degradation into abundance.

Sustainable Maritime Fuels: Trends in LNG and Hydrogen Adoption for Global Trade Routes

As the global shipping industry navigates the choppy waters of climate imperatives, a profound shift toward low-carbon fuels is underway. Traditional heavy fuel oil (HFO), long the workhorse of maritime propulsion, is giving way to cleaner alternatives like liquefied natural gas (LNG) and hydrogen. Driven by stringent regulations from the International Maritime Organization (IMO) and the European Union’s Emissions Trading System (ETS), this transition promises to slash emissions while reshaping trade dynamics. In Asia’s bustling corridors—from the Malacca Strait to the Bay of Bengal—these fuels are gaining traction, with forecasts pointing to a 15% surge in green vessel deployments by the end of 2026. Bangladesh, with its strategic ports, emerges as a potential bunkering powerhouse. Drawing on insights from IRENA and BIMCO reports, this feature explores the trends, challenges, and opportunities fueling this green revolution.

Regulatory Catalysts: IMO and EU ETS Pushing the Envelope

The push for sustainable fuels stems from escalating regulatory pressures. The IMO’s revised 2023 Greenhouse Gas (GHG) Strategy, updated with net-zero ambitions in 2025, mandates a 20% reduction in shipping emissions by 2030, 70% by 2040, and net-zero by around 2050 compared to 2008 levels. This includes carbon intensity cuts and a proposed Net-Zero Framework with mandatory fuel standards and GHG pricing, set for final adoption in 2026 and implementation from 2028. Delays in voting have raised concerns, potentially stalling clean fuel projects, but the framework emphasizes low-carbon options like LNG and hydrogen-derived fuels.

Complementing this, the EU ETS extended to shipping in 2024, covering CO2 from large vessels, with methane and nitrous oxide added in 2026. By 2026, operators must surrender allowances for 100% of emissions, up from 70% in 2025, leading to surcharges that could add 12% to freight costs. FuelEU Maritime, effective since 2025, further mandates gradual GHG intensity reductions in marine fuels, promoting renewables and low-carbon alternatives. These rules are accelerating adoption, with non-compliance penalties incentivizing a switch from fossil fuels.

LNG and Hydrogen: The Front-Runners in Low-Carbon Propulsion

LNG, a transitional fuel, dominates current trends due to its availability and infrastructure. It reduces GHG emissions by up to 23% on a well-to-wake basis compared to HFO, with even greater cuts in SOx (nearly 100%) and NOx (up to 80%). However, methane slip remains a concern, prompting advances in bio-LNG and e-LNG for deeper decarbonization.

Hydrogen, particularly green variants produced from renewables, offers near-zero emissions—up to 95% GHG reductions when used in fuel cells or as derivatives like ammonia and methanol. IRENA highlights green hydrogen as the backbone for shipping’s net-zero pathway, with derivatives like ammonia potentially meeting 95% of energy needs by 2050. Challenges include high costs, low energy density requiring larger storage, and limited infrastructure, but innovations in value chains are bridging gaps.

To compare, here’s a table of emission reductions for key fuels (well-to-wake basis, relative to HFO):

Asia’s Trade Corridors: Hotspots for Fuel Adoption

Asia, handling over 40% of global maritime trade, is a focal point for sustainable fuel rollout. Corridors like the South China Sea and Malacca Strait, vital for energy imports, face heightened risks from emissions regulations. LNG bunkering is expanding in Singapore and Japan, while hydrogen pilots emerge in South Korea and China. BIMCO notes biofuels and LNG as interim solutions, with hydrogen gaining for long-haul routes. Costs remain a barrier: LNG is competitive at $500-1,000/ton, but hydrogen could be 2-3 times pricier without subsidies.

A comparative table of fuel costs (2026 estimates, USD per ton, including compliance):

2026 Forecasts: Surging Green Vessel Deployments

Forecasts for 2026 predict a 15% rise in green vessel deployments, driven by order books and regulations. BIMCO reports over 500 alternative-fueled container ships on order, representing 53% of newbuilds, with deliveries ramping up. Overall, sustainable fuels could capture 5-10% market share by 2026, up from <2% today, per IRENA and market analyses. The sustainable marine fuels market is projected to hit $19.86 billion in 2025, growing at 52% CAGR.

Market share table (global shipping fuel mix, 2026 forecasts):

Bangladesh’s Emerging Role in Bunkering Hubs

Bangladesh stands poised to capitalize on this shift, with ports like Chittagong and Matarbari eyed for LNG bunkering. Studies highlight potential for FSRU-based facilities, leveraging existing LNG imports to serve regional trade. As a gateway for South Asian routes, it could become a hydrogen hub with investments, aligning with global zero-carbon bunkering trends. The transition to sustainable fuels is not just environmental—it’s economic. By 2026, Asia’s corridors could lead the way, with Bangladesh at the helm.

Expanding Bangladesh’s Bunkering Case Studies: LNG and Hydrogen in Focus Building on the potential highlighted in the sustainable maritime fuels landscape, Bangladesh’s strategic position in the Bay of Bengal positions it as an emerging player in bunkering for low-carbon fuels. With ports like Chittagong and the developing Matarbari deep-sea facility, the country can leverage its growing LNG import infrastructure and nascent hydrogen exploration

to serve regional and global trade routes. Below, we delve into detailed case studies drawn from recent analyses, focusing on LNG bunkering viability and hydrogen applications in maritime vessels. These examples underscore economic opportunities, environmental benefits, and implementation challenges, supported by data from key reports and studies.

Case Study 1: LNG Bunkering Potential at Chittagong and Matarbari Ports

A comprehensive 2023 study (updated with 2025 insights) on the feasibility of LNG-fueled ship bunkering in Bangladesh evaluates Chittagong and Matarbari as prime sites for establishing dedicated facilities. This analysis, grounded in port capabilities, trade patterns, and regulatory alignments, projects Bangladesh could capture bunkering demand from vessels trading with Emission Control Areas (ECAs) in Europe, North America, and Asia.

- Project Overview and Sites: Chittagong Port (coordinates: 22.3091°N, 91.8018°E), Bangladesh’s main gateway handling over 3.5 million TEUs annually, supports vessels up to 190m in length and 9.5m draft. It currently lacks dedicated LNG bunkering but

benefits from proximity to existing Floating Storage and Regasification Units (FSRUs) like the Moheshkhali terminal. Matarbari Port (21.6914°N, 91.8590°E), under development as a deep-sea hub, accommodates larger ships (up to 338m length, 16m draft, suitable for 10,000 TEU vessels). It integrates with planned LNG terminals, including Summit Group’s FSRU project, which faced termination threats in 2025 but was urged for reconsideration to boost capacity. Additional sites like Kuakata and Bhola are eyed for expansion, leveraging offshore gas reserves. - Economic Viability: Bangladesh’s exports to ECA zones (e.g., U.S., Germany, UK) totaled $204.65 billion in 2021-2022, with six of the top 10 importers in regulated areas. Direct routes via Matarbari could reduce transshipment via Singapore or Sri Lanka, attracting LNG-fueled vessels. With global LNG-fueled ships at 251 operational and 403 on order (projected bunkering ports rising to 200 by 2024), Bangladesh could generate revenue through competitive pricing. Onshore reserves (high reserves-production ratio) and imports (projected 115 cargoes in 2026, up 5.5% from 2025) ensure supply. A World Bank loan guarantee of $350 million in 2025 eases import costs, supporting bunkering economics.

- Environmental and Operational Benefits: LNG cuts emissions by 90% SOx, 80% NOx, 100% particulate matter, and 20% CO2 versus heavy fuel oil (HFO), aligning with IMO 2020 sulfur caps and ECA expansions (e.g., China and South Korea in 2022).

- Challenges: No existing bunkering terminals lead to reliance on regional hubs like Cochin (India) or Busan (South Korea). Infrastructure gaps include mooring systems, spill containment, and safety protocols. Trade dependencies on indirect routes and environmental risks (e.g., spillage) pose hurdles. Rising LNG spot prices and domestic gas shortages (driving 2025 imports) could inflate costs.

- Recommendations and Outlook: The study urges rapid infrastructure development at both ports to exploit geographical advantages and growing demand. By 2026, with Matarbari operational, Bangladesh could position itself as a cost-effective alternative to Asian giants, potentially handling 15 million mt/year of LNG imports amid 6-7% GDP growth. Integration with offshore gas extraction and FSRU expansions is key for sustainability.

To quantify viability, here’s a comparative table of port capabilities for LNG bunkering:

(Data adapted from feasibility study and port reports.

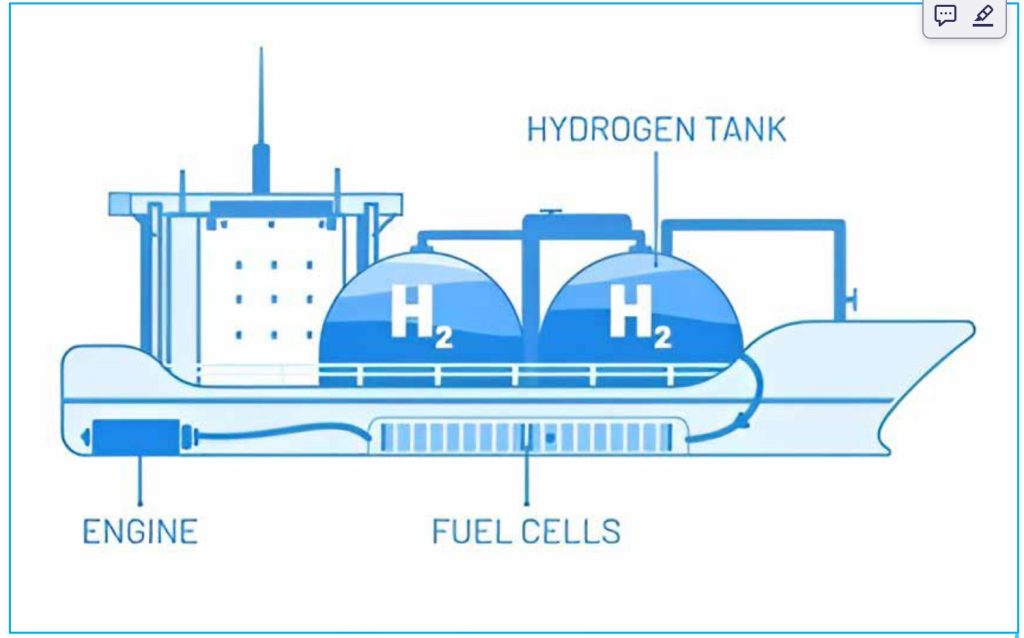

Photo: The Hy-Ekotank concept, launched by TECO 2030 and partners Ektank AB

Case Study 2: Hydrogen-Powered Inland Oil Tankers – A Feasibility Analysis

While ocean-going hydrogen bunkering remains nascent in Bangladesh, a 2023 case study on life cycle analysis of hydrogen-powered marine vessels provides insights through comparisons of inland oil tankers operating on domestic routes.This research evaluates hydrogen fuel systems against conventional diesel, highlighting potential for bunkering in riverine and coastal areas, amid broader discussions on zero-carbon fuels in developing countries.

- Project Overview: The study analyzes fuel systems for oil tankers on Bangladesh’s inland waterways(e.g., routes along the Meghna and Padma rivers).It compares conventional diesel engines with hydrogen fuel cells and internal combustion engines (ICE),using real-world data from operational tankers. Hydrogen is considered as compressed gaseous or liquid forms, with bunkering simulated via truck-to-ship or small-scale terminals at ports like Mongla or Payra.

- Economic Viability: Hydrogen systems show higher upfront costs (2-3 times diesel setups due to storage and fuel cells), but long-term savings from lower maintenance and fuel efficiency. A U.S.-based parallel study notes total cost of ownership (TCO) for hydrogen vessels could double diesel at $10/kg H2 prices, but drops with scaling. In Bangladesh, subsidies and green hydrogen production (e.g., via renewables) could make it viable by 2030, especially with EU ETS influences on exports.

- Environmental Benefits: Hydrogen achievesnear-zero emissions (95-100% GHG reduction vs.

diesel), with zero SOx/NOx/PM. The analysis quantifies life-cycle emissions: diesel tankers emit ~1,200 kg CO2 per trip, while green hydrogen cuts this by 90%+. This aligns with IMO net-zero goals and could extend to coastal bunkering. - Challenges: Limited infrastructure—no dedicated hydrogen bunkering exists, with risks in storage (low energy density requiring larger tanks) and safety (flammability). Feasibility is lower for long-haul due to refueling needs; inland routes are more practical. High production costs ($2,000-4,000/ton) and supply chain gaps hinder adoption.

- Recommendations and Outlook: Scale pilots on inland vessels before ocean expansion, integrating with ports like Chittagong for hybrid LNG-hydrogen hubs. World Bank reports suggest developing countries like Bangladesh prioritize ammonia (hydrogen-derived) for bunkering, with investments in $1.4-1.9 trillion global needs. By 2026, with rising green vessel deployments, Bangladesh could pilot hydrogen bunkering at Matarbari.

Comparative table of fuel systems for Bangladesh inland tankers:

(Data from life-cycle analysis.)

These case studies illustrate Bangladesh’s pathway to sustainable bunkering, blending immediate LNG opportunities with long-term hydrogen potential. Investments in infrastructure and policy alignment could yield billions in trade benefits while advancing decarbonization.

Study of the Potential of LNG Fueled Ship Bunkering System in Bangladesh – ResearchGate (2025) – https://www.research-gate.net/publication/370675285_Study_of_the_Potential_of_LNG_Fueled_Ship_Bunkering_System_in_Bangladesh

Bangladesh: LNG imports from long-term suppliers to rise54pc in 2026 – Hellenic Shipping News (2026) – https://www.hellenicshippingnews.com/bangladesh-lng-imports-from-long-term-suppliers-to-rise-54pc-in-2026

World Bank helps Bangladesh with pricey LNG imports – Gas Outlook (2025) – https://gasoutlook.com/analysis/world- bank-helps-bangladesh-with-pricey-lng-imports

INTERVIEW: Bangladesh LNG imports may hit 15 mil mt/ year on economic growth: Summit Chairman – Summit Power International (2025) – https://summitpowerinternational.com/interview-bangladesh-lng-imports-may-hit-15-mil-mt-

year-economic-growth-summit-chairman

Bangladesh Boosts Spot LNG Imports Amid Gas Crunch – Energy Intelligence (2025) – https://www.energyintel.com/0000019a-3f7c-ddaf-ab9f-bf7f55680000

Life Cycle Analysis of Hydrogen Powered Marine Vessels—Case Ship Comparison Study with Conventional Power System – ResearchGate (2023) – https://www.researchgate.net/publication/373474804_Life_Cycle_Analysis_of_Hydro-gen_Powered_Marine_Vessels-Case_Ship_Comparison_Study_with_Conventional_Power_System

The Potential of Zero-Carbon Bunker Fuels in DevelopingCountries – World Bank (2021) – https://documents1.world-bank.org/curated/en/110831617996384433/pdf/The-Poten-tial-of-Zero-Carbon-Bunker-Fuels-in-Developing-Countries.pdf

An Extensive Review of Liquid Hydrogen in Transportation with Focus on the Maritime Sector – MDPI (2022) – https:// www.mdpi.com/2077-1312/10/9/1222

Decarbonizing the Maritime Industry: An Opportunity to Further Indonesia’s Just Energy Transition – Center for Global Development (2023) – https://www.cgdev.org/publication/decarbonizing-maritime-industry-opportunity-indonesia-just-energy-transition

A pathway to decarbonise the shipping sector by 2050 – IRE-NA (2021) – https://www.irena.org/-/media/Files/IRENA/Agency/Publication/2021/Oct/IRENA_Decarbonising_Shipping_2021.pdf

Shaping sustainable international hydrogen value chains -IRENA (2024) – https://www.irena.org/-/media/Files/IRE-NA/Agency/Publication/2024/Sep/IRENA_Shaping_sustainable_hydrogen_value_chains_2024.pdf

More than 500 alternatively-fuelled container ships now on or-der – BIMCO (2025) – https://www.bimco.org/news-insights/market-analysis/shipping-number-of-the-week/2025/0918-snow

IMO approves net-zero regulations for global shipping – IMO(2025) – https://www.imo.org/en/mediacentre/pressbriefings/pages/imo-approves-netzero-regulations.aspx

Reducing emissions from the shipping sector – EU Climate Action – https://climate.ec.europa.eu/eu-action/transport-decarbonisation/reducing-emissions-shipping-sector_en

INSIGHT: A Comparative Analysis of Alternative Fuels for Sustainable Maritime Shipping – Ship & Bunker (2025) – https://shipandbunker.com/news/world/527976-insight-a-com-parative-analysis-of-alternative-fuels-for-sustainable-mari-time-shipping

Sustainable Marine Fuels Market Size, Share & Growth, 2033 – Market Data Forecast (2025) – https://www.marketdatafore-cast.com/market-reports/sustainable-marine-fuels-market